Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Buying A Home For $659 Down – A Case Study

As a Real Estate Broker in the business for the last 7 years I’ve noticed a growing trend on the social media front, on the news/entertainment front, among my peers and my own wallet. The cost of living has increased and home affordability is becoming a problem for a large swath of the would be “First Time Home Buyer” population.

It totally makes sense! The cost of goods and services has increased pretty dramatically over the past few years especially. Incomes haven’t exactly risen to match. I do have an article I wrote diving deeper into the cost of living topic. If you’d like to read that you can view it HERE. If you’re in the Gen Z or Millennial age group, this growing issue probably hits pretty close to home. You may have parents that have owned a home for a very long time and are reaping the benefits of long term home ownership. You may also be wondering if that’s even a possibility for you…

Well… depending on your circumstance, if you can come up with a thousand bucks, I am here to tell you that it is a possibility! As a matter of fact we were able to do just that for one of my first time home buyer clients this week!

Meet Nate

This is Nate. He’s 22 years old and seems to like Dinosaurs a lot!! He falls into the Gen Z first time home buyer category almost perfectly. Nate has a full time job that pays ok, but was going to need some help coming up with a down payment for his first home. What Nate lacked in funds, he MORE than made up for in willingness to learn and roll up his sleeves to get the job done. I should note that Nate is my nephew, but I didn’t do anything above and beyond what I’d do for any of my clients. He didn’t get any special treatment. If anything I was a bit harder on him lol.. Lets get into it shall we?

Getting Pre-Approved

The first step you should take when getting ready to buy a home is to talk to a lender and see where you land. Your Realtor will point you in the right direction. Window shopping is fun and all, but if you don’t know what you can afford you should definitely keep you search limited to online browsing. Nate was an eager buyer and ready to learn. He wasted no time at all and got in touch with several lenders and ended up landing on one he liked.

Nate was able to qualify for a “First Time Home Buyer” grant in the amount of $7500.00. This was a tremendous help for him. Frankly it was the “Linchpin” to the whole process. Funding for this program is limited and is usually given out on a first come first serve basis. To see if you qualify I recommend you reach out to a lender or read more about it HERE. Nate ended up qualifying for a 3.5% down FHA loan. I’ll explain why that’s important shortly.

The Home Search

Nate’s purchase price cap was 150k max, a common First Time Home Buyer price. For those of you that haven’t been in the home search process here in Lincoln, that is a difficult price point to find a home and even more difficult to buy. Particularly if you don’t want it to be a piece of junk. For a properly priced and marketed home OF ANY KIND in this price point it’s not uncommon for the seller to receive 20+ showings and 10+ offers in a 48 hour time frame. It’s simple supply and demand. As home values have increased along with interest rates, debt has become more expensive. Making these price points crowded. You just can’t build this stuff for cheap anymore. So the existing inventory is what we got.

To compound our home search difficulty Nate was an FHA buyer. It’s not a bad loan program, it’s a great program for any first time home buyer. It actually comes with an added layer of protection for the buyer in the form of a conditioned based appraisal. Meaning if an issue was found, the loan wouldn’t close until the issue was fixed. Where that becomes a problem is competing with multiple offers at this price point. Typically it’s an “all cash” or “conventional loan” with no inspections that ends up being the winning offer in these price points.

So straight away I told Nate we were going to have to think outside the box to find him a home. I also told him that it was a near certainty that he was going to have to put in some work on whatever home we found to make it pass the FHA inspection / appraisal. He was completely fine with that so we pressed on.

Looking “Off Market”

Given Nate’s search criteria and financing I new right away that we’d never be able to compete on the open market at this price point. We didn’t even bother to look. Instead we limited our search to off market listings. By “Off Market” I mean properties that are either listed “For Sale By Owner” (FSBO for short) or not listed at all. In my opinion, looking at properties in this category can give you a real leg up in the negotiations. In my previous experience of working with FSBO’s they typically don’t have as much knowledge on current market conditions and what their home ought to bring on the “Open Market”. To read more on the disadvantages of selling “For Sale By Owner” click HERE. To make any deal work for my client, we were going to have to do some negotiations that the “Open Market” just wouldn’t bear.

After a couple weeks of searching off market our “Diamond in the Rough” appeared. This property was a perfect fit for Nate. It was in his desired neighborhood, had a newer foundation, roof, siding and windows. I’d say it needs a cosmetic rehab but was perfectly livable in it’s current condition. The best part? It was under priced. I did notice some peeling paint and a cracked window that wouldn’t pass inspection so I knew that was going to be an issue, but Nate was up to the task.

Negotiations

After determining that Nate wanted to move forward on this one we drafted up an offer. We ended up offering asking price with a $3000.00 credit to the buyer for down payment assistance. We also asked for any consumables / supplies we’d need to facilitate any FHA repairs that may come up. In return, my buyer would facilitate as many repairs as he was capable and would hire out the rest. The seller accepted our terms!

Once it was all said and done between the $3000.00 dollar credit from the seller and the $7500.00 grant, Nate actually had a surplus of money. He was required to have $250.00 of his own money into the transaction. So he had some money to play around with.

Repairs

The FHA appraisal confirmed my suspicions that Nate was going to have to do some work to make the home pass inspection. It even turned up a couple minor items I missed (hey I’m not perfect lol…). The bulk of the work was comprised into 2 jobs. Repainting the entire garage and replacing a cracked window in one of the bedrooms. Luckily Nate has a pretty awesome uncle with a bunch of tools sitting around. Again, no special treatment. I made him do it all. For the record, if you were my client I’d lend you my tools too.

The garage was a 2 day project and Nate determined that power washing it was the most effective way at getting all the paint chips off. It’s also good practice to clean the surface to prep for paint. The power washer took care of 95% of the chipped paint and a scraper did the rest. To save him a little trouble I lent him my spray gun too. I don’t think he’s in danger of being a professional painter any time soon but it was good enough to pass inspection.

The window was a pocket style window which is about as easy as they come to replace. The whole job took about an hour.

Closing

After repairs were completed the appraiser came back out and gave it his stamp of approval. The next week Nate ended up closing on the house and I think he got himself a pretty good deal and a home I believe will suit his needs for quite a while. All for just $659.75 of his own money. We ended up applying the surplus to principal pay down. Prior to doing this transaction I always thought you needed to have $1000 of your own money into the deal with the first time home buyer grant. It just goes to show I learn something new as well with every person I help.

Nate already has a buddy that’s agreed to move in with him and pay him rent. After it’s all said and done, he’ll be paying less for his mortgage than he was paying for rent. Something I’m sure he appreciates.

You Should Do This Too!

The reason I wrote this article is to show you that home ownership is within your grasp. If you’re like me, you probably spend way too much time on social media. One of the big things that I continue to see is how “Our” generation is screwed. First we went through the “Great Recession”. Then we couldn’t get a job with our over priced bachelors degree in “Underwater Basket Weaving”. Then house prices got out of control. Don’t let this stuff get in your head. That’s a victim mentality. If you want to own and home, there is a way to make it happen. If you have a job above minimum wage and a thousand bucks then you can do it too. Don’t have a thousand bucks? Sell some stuff. Most people have more than they ACTUALLY need.

This is a duplicatable strategy. I’ll be the first to admit. Deals like this just don’t fall out of the sky, but they are out there. If you align yourself with the right people, you can be a home owner too. And if once you start the process and run into some road blocks, keep going. Fix whatever that issue is, and keep going. Don’t give up!

-Cody & Jos-

Selling For Sale By Owner? Some Things To Consider

Way back in 2015 I was a first time home flipper, full of ambition with an “I know what I’m doing” attitude. I watched “Flip or Flop” a time or two… How hard could it be?? My business partner and I were putting the finishing touches on a house we had just got done remodeling. Our plan was to sell it For Sale By Owner to save money. We were in uncharted territory when it came to marketing a house. Frankly we didn’t have a clue what we were doing. We figured we would throw some pictures up on Zillow using our potato phone (camera phones sure have improved since then) and the offers would just come pouring in!!

They didn’t. We overpriced our listing, took awful photos, weren’t properly marketing the property and we were emotionally attached since this was our first flip. Who cares what the comparable sales say right? Fast forward about 2 months and we enlisted the help of a Realtor. The property ended up selling right at what the comps were showing, in relatively short order.

Fast forward to present day and I have since gotten a “Baptism by Fire” education on exactly what it takes to sell a home. Having been in the business since late 2016, I’ve been apart of the sale of well over 100 homes. I also see on a daily basis other for sale by owners making the exact same mistakes I was making back in 2015.

Buckle Up! We’re going to school

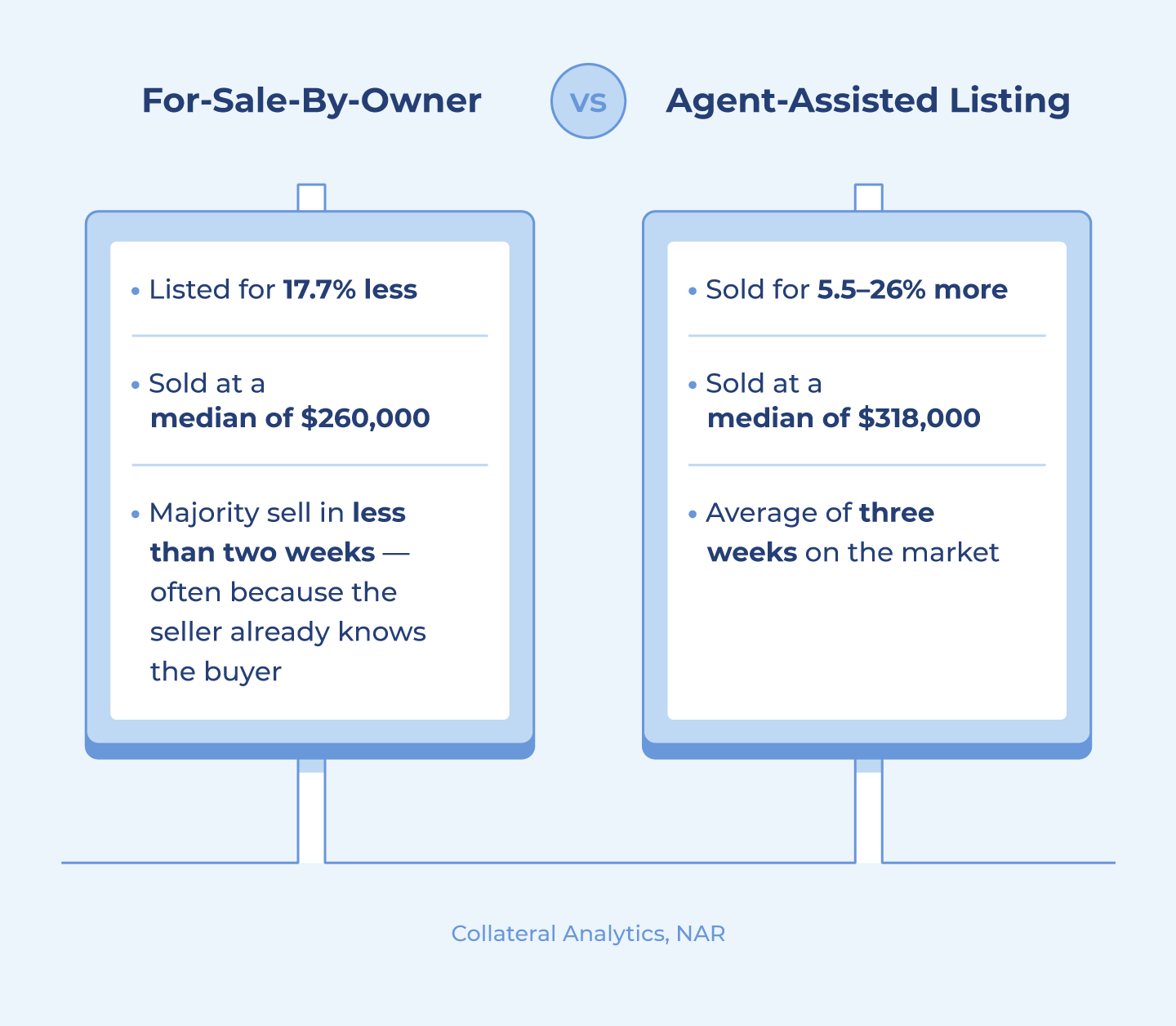

Now I don’t want to say it’s impossible to sell a home without the assistance of a Realtor. But the odds are stacked against you and it’s likely gonna for sell for less… At least that’s what the data shows.

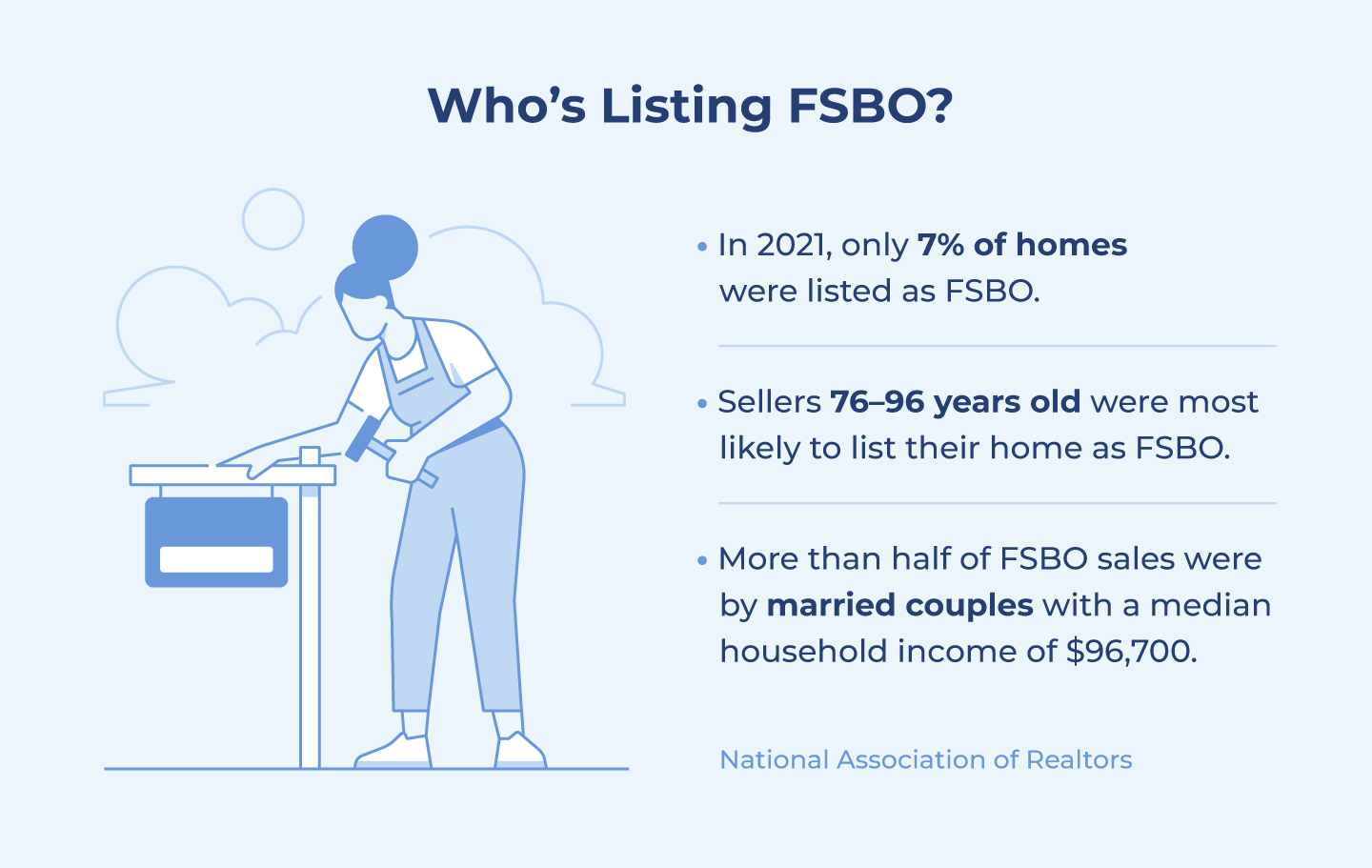

According to the National Association of Realtors 2021 analysis of all FSBO vs Realtor sales, there is a stark contrast between what a for sale by owner listing vs a Realtor listing will sell for. The average sales price for all FSBO sales is 260k. The average sales price for a Realtor assisted sale is 318k. I will concede that for sale by owner on average did sell faster. For that kind of a bargain I can see why. To add some context, for sale by owner listings made up 7% of all real estate sales in 2021, down from their high of 15% back in the early 1980s.

Now I think there are a lot of reasons for this. Some I can back up with stats, and some anecdotal evidence that I’ve seen though out the years. Lets get into it shall we?

FSBO’s Get Less Exposure

This is probably THE most important factor when it comes to selling a home. Realtors have a pretty big leg up against FSBO’s on this one. Whenever we list a property on our Multiple Listing Service (MLS for short) our listing automatically gets input onto literally thousands of websites. If it’s a website where you look at real estate, you will find it there. A FSBO would have to manually input all those listings into each website individually to match the exposure we offer.

On top of that, a good realtor is going to take the time to put together a comprehensive marketing strategy. Some examples of this include:

- Professional Photography (this is beyond important)

- Videography

- Staging

- Direct mail marketing campaign

- Social media marketing campaign

- Agent, Office and Client open houses

- Word of mouth (we’re in the business and probably know a buyer or 2 for your place)

And honestly so much more than that. Marketing a listing deserves it’s own blog post! I guess I know what one of my future articles is going to look like…

You’re typically priced wrong

I keep a pretty close eye on the For Sale by Owner market for 2 reasons. The first is for my buyers. This is a pool of inventory that a lot of agents don’t utilize. This is a good thing for my clients and I’d be doing them a disservice if I wasn’t. Some of my first time buyers are having a hard time competing with the agent listed properties and the multiple offers they typically receive. Just last week we were able to get one of my buyers under contract on a FSBO listing under 150k while getting money back at closing at a price under it’s market value. Ask any Realtor worth their salt and they’d probably tell you that’s not happening on a correctly priced and marketed agent listed property in this market.

The 2nd reason I keep a close eye on the for sale by owner market is for future business. Full transparency, I’m trying to help you and usually you’re making the same mistakes I was making back during my first flip. You’re usually over priced and I completely understand why as well. “It’s my house it has to be worth more.” Typically the FSBO listings that sit on the market longest are the properties that are over priced. Nine times out of ten these properties are listed with agents in about a month to 6 weeks. I’m not the only one calling you. The underpriced homes will typically sell in short order. Kind of gives credence to the FSBO stats I listed above. Be sure not to trust online home value calculators. They can definitely lead you astray. For more info on that, read my article here.

Some Realtors won’t show your listing

I’m going to say the quiet part out loud. Most Realtors don’t like working with FSBO’s. The problem is they’re unsure if you as a FSBO is willing to pay them to bring you a buyer. If you’re still on the fence about using a Realtor, you probably think this is a good thing. I understand why you would. Why pay a pesky Realtor when you can save money on the commission. “I can find my own buyer”. Here’s something you probably haven’t considered…

As a whole, the Real Estate sales industry has done a very good job of educating the general public that working with a Realtor to buy a home costs a buyer very little, and under certain circumstance, nothing at all. It’s an easy sales proposition. Work with a Realtor and they will watch your back when buying a home. It costs very little. This is especially true for first time home buyers. Having never been through the sales process they’re usually going to want someone to cross all the T’s and dot all the I’s so to speak. As a buyers agent we get paid from the commission that’s pre-negotiated from the Listing agent’s commission structure.

At the very least, if you insist on selling “For Sale by Owner” include some language in your listing description stating that you cooperate with buyer’s agents. Some of the bolder agents will approach you. Something to think about though. You will be paying an agent (likely a skilled one) to negotiate against you. If you’re willing to go that far, you may as well pay an agent to represent your best interest. Statistically speaking it’s very likely you’ll end up netting more in the long run.

Story time

A few years back I was helping a client that was previously trying to sell their home for sale by owner. They were in the process of building a new home and needed the proceeds from the sale of their current home to close on the new one. They hadn’t received an offer and had little traffic on their place. I took over the listing utilizing the marketing strategies I mentioned above and started to get traffic into the home. (Actual house pictured below.)

My client had a ring door bell and this was before they had mass adoption in our market. My client sent me the video of what the buyers agent had discussed with their buyer. I’m paraphrasing a bit but it went something like this: Agent “Did you like the home”? Client “I sure did, it’s a perfect fit for what we need.” Agent “Excellent! I’m glad you like it. I actually saw this when it was a for sale by owner but I wasn’t sure if they cooperated with agents. I’m glad it got listed because when I saw it I knew this was the perfect place for you!”

Later that evening we received a great offer from that agent and went under contract. My client was very upset knowing that at least one agent saw this and refused to show it when it was a FSBO. He got over it once he moved into his new house though…

You’re waiting for an unrepresented buyer

Despite our industries attempts at educating the buyer pool, there are still a small percentage of buyers that work without a Realtor. These are usually savvy investor types in my experience. There is a very specific reason they don’t work with Realtors. They’re looking for a deal. Most Realtors work in retail priced real estate. They’re entire niche is finding homes that aren’t properly marketed and lingering for sale. Then they will come in with a low ball offer in an attempt to scoop up a deal.

If you’re holding out hope for that one perfect buyer that’s unrepresented willing to pay full asking price, you might be waiting for a while. I’m not saying it can’t be done, it’s just a lot less likely. Particularly if you’re selling in the 300k and under price point in our market. The current market we’re in is all about speed. The longer your listing sits, the less likely it will sell for market value based solely on buyers perception. “Why has this been sitting for so long? Is something wrong with it?”

We handle it all from “Keys in our hands” to “Check in your hands”

There are a LOT of things that need to go right in order for a home to sell at it’s maximum value. If all those things don’t line up perfectly, it will typically result in a lower sale price, or no sale at all. We’re trained specifically to facilitate a sale, recognize any potential pitfalls along the way and mitigate those pitfalls. Some of those we’ve learned from our colleagues in the business and others we’ve learned through the school of hard knocks. Unless you are a sophisticated investor with dozens of sales under your belt, it’s likely you won’t have the same experience that we have as Realtors working in the business every day.

In summary – Yes, you can sell your house on your own, but it’s highly likely we will end up netting you more money in the long run. Unless your last name is Bezos or Musk, it’s likely that the extra money will help make a difference in your life. I know you were just trying to save money, but you will make more with us.

-Cody & Jos-

Renovations To Consider For Increasing Your Home’s Value

Every time I walk through a house I’m always looking at ways to maximize the value of the home. It’s just something that’s engrained in me. I can’t help myself. I cut my teeth in the real estate world by doing renovations to beat up rentals and doing house flips. That eventually transitioned into being a short term rental operator and being a real estate broker. I guess those skills have a bit of utility on my current path.

The type or scope of the renovations you’re going to do should depend ALOT on what your goals are. If you’re planning on sticking around for the long term, I say go wild! I don’t personally recommend painting your cabinets salmon or going with turquoise countertops or anything like that. But the longer you’re sticking around the more likely you are to recoup your investment on the remodel in the form of equity.

Time To Get Your Home Photoshoot Ready

If you’re planning on doing a spruce up on your home for the purpose of resale, I highly recommend you keep the design theme neutral. Trends come and go. Those “Golden Oak” cabinets that were so cool in the 90’s make your house look pretty dated now. You can be a little brave with your design, but not too brave!

Another thing you need to take into account is what the end value of you home is going to be worth and what your neighborhood will support for that value. That last thing you want to do is waste money on renovations that aren’t going to pay you back. You probably don’t need $75 sq ft Quartz countertops in a neighborhood where the highest comp is 175k. Laminate countertops will be fine. If you’re having trouble figuring out what your renovated value should be, give your friendly neighborhood realtor a call. Don’t trust the online value calculators like Zillow’s “zestimate”. If you want some ammo on why those can be WAY off – READ MY ARTICLE ABOUT ZILLOW’S ZESTIMATE.

FULL DISCLAIMER – I am not an interior designer. I’m just a guy that sells real estate and pays attention to what sells and what doesn’t. With that out of the way, lets get into it. I’ll try to keep this in order of least expensive to most expensive.

Clean and De-clutter

This is such low hanging fruit that I almost didn’t want to include this on the list. You can hardly call this home renovations, but it unlocks otherwise hidden value. I see listings all the time where owners don’t take the time to do this. This is a requirement, not a recommendation. If you’re working with a Realtor and they don’t mind listing a dirty home, that should give you pause. It costs you almost nothing but your time. If your time is limited, hire a cleaner. Seriously. It’s that important.

Paint and Update Fixtures

This has such a good “bang for the buck” value that it’s probably a glitch in the matrix. Whenever I have clients that are a bit adventurous, but not too handy, this is the step I recommend. If you’re just painting the interior of a house you can probably do this yourself for around $500.00. Tack on fixtures like door handles, lights and cabinet pulls and this can really transform the look of your house on a meager budget.

Landscaping

First impressions are everything, and what screams “I have my life together” better than a well-manicured lawn? I don’t think you need to get too crazy with this either. So long as the grass is cut, branches are trimmed and your hasta plants aren’t dead I think you’ll be fine. Mulch goes a real long way too. I myself don’t have much of a green thumb… that’s why I have rock in my flower beds. Even I haven’t found a way to kill those yet.

“Legalize” Your Illegal Bedrooms

This is one of my favorite renovations. We’re starting to get a bit up there in the “spendy” category but I’ve never had a client lose money on this strategy. I do recommend you hire this one out, it takes some gnarly equipment to cut a hole in a basement wall. The cost to do this ranges between $2,500 – $3,500 but at a minimum you’re going to double your money by adding legal bedrooms. There is one caveat to this. The less bedrooms you have to start the better. If you currently have 2 bedrooms and you “legalize” a 3rd, you’re going to get the most value out of that. If you have 6 bedrooms already and “legalize” a 7th, you’re not going to get as much back for that 7th bedroom. Law of diminishing returns… or something like that.

Flooring

New carpet, tile and flooring go a LONG way to improve the feel of your home. This is another one of those categories where it’s a bit “spendy” though. Laminate flooring is relatively easy to install with a few basic tools if you’re feeling handy. There are cost effective options on laminate flooring as well. Dingy carpets will definitely scare buyers away. At the very least you might be able to get away with cleaning them. If there too far gone, it’s best to replace them.

Kitchen and Bathrooms

Kitchen and bathroom updates. You didn’t think I was going to forget this one did you?!? What home renovations list would be complete without mentioning kitchens and bathrooms! I know you’ve heard this on HGTV a million times that “Kitchens and bathrooms sell the home” but it’s so true! Generally speaking this is about the most expensive thing you can do on this list. That doesn’t mean you can’t make a big visual impact on a meager budget though. Especially if you’re willing to roll up your sleeves.

I’ve got another disclaimer – I’m not a licensed contractor either, I’m just fairly handy. Here’s an example of a kitchen remodel we did last year on one of our places. It started out life as a builder basic 90’s Golden Oak special. We swapped out the counter tops, redid the back splash, painted the cabinets, removed some upper cabinets and added a shelf. All in on this we spent just a shade over $4,000.00 to achieve this look. Now, I know what you’re thinking – “Cody, I thought you said don’t pick any funky colors?? Those cabinets look like a John Deere Tractor?!?” Here’s what I have to say about that. This was designed to stand out because we use this property as an Airbnb and wanted it to attract attention. Best thing I can say is “Do as I say, not as I do”.

I Feel A Conclusion Brewing…

To sum things up, unless you live in a brand new house it’s likely that you’re leaving some meat on the bone in the form of equity. There are lots of ways you can increase the value of your home. Some are listed above, there are still others I didn’t mention. And here’s the tricky part, even if you’re looking to sell soon sometimes it doesn’t make sense to do those renovations, but sometimes it does. That depends on a lot of things like your budget, motivations for selling, timeline etc… Frankly, that’s a discussion for another article.

If you’re curious to know what your home is valued at and whether it’s worth it to spruce it up or leave well enough alone, feel free to reach out to either of us. We would love to be of assistance.

-Cody & Jos-

Real Home Value Vs Zillow’s “Zestimate

Zillow knows what they’re doing, right??

Last week, Jos and I were showing properties to one of our clients and we came across one that she was very interested in. It checked all the boxes. Nice neighborhood, plenty of space, HOA to take care of lawn and snow and most importantly at a price she could afford as a single mother. Ultimately she decided she wanted to write up an offer. After we gave her our estimated home value & offer amount she was a bit perplexed… She said “But the Zestimate on this is only 171,000”.

As Realtors, we know that Zillow’s “Zestimate” is generally speaking somewhere in the ballpark, but not the end all be all of home values. If I’m speaking Mandarin to you, let me break it down. Zillow is probably the premier website for home searches that the general public is aware of. They have what’s called a “Zestimate” for most homes. This is their proprietary algorithm that they use to derive an “estimated home value” of a given property.

For the record, our CMA or “Comparative Market Analysis” on this particular property came in right around the $205,000 mark. It’s not like this property was in some super unique neighborhood. We didn’t have to make a ton of adjustments to derive a value. This home was a townhome located in a neighborhood with 40 or so identical townhomes with recent sales to support value. As far as CMA’s go, this one was a “lay up”!

The Plot Thickens…

Too add some fuel to the fire of the “Zestimate” inaccuracies, I want to give you a brief history lesson. Back in April of 2018, Zillow launched a program called “Zillow offers” where Zillow would offer to buy your home. This programs was launched in 24 markets around the country. Mostly larger metropolitan areas like Los Angeles, Cincinnati, Orlando, Phoenix and places like that. They would use their “Zestimate” as the basis for what kind of price to pay for these homes that they purchased.

Their end goal was to buy properties quickly for a discount, do an HGTV style remodel on them then turn around and sell them back to the general public. Just in case you haven’t been paying attention to home values going back to 2018 you should know that home values nationally have increased quite a bit since that time. I’ll explain why that’s important in just a minute.

The Plot Thickens… but more this time….

Fast forward to 2021 and Zillow’s home purchasing program has ran aground. Their total 2021 losses in Zillow’s home flipping venture amounted to $881,000,000.00. That’s nearly a billion dollars, with a “B”. Meanwhile, if you were a home owner during the late 2020 to late 2021 time frame you probably saw a home value increase of around 17.5%. These are national figures, so each market is going to be a bit different. I don’t want to make the same mistake that Zillow did lol… Long story short, Zillow managed to lose money flipping homes in a rising market utilizing their “Zestimate” as the basis for purchasing these homes.

Adding insult to injury, Zillow decided to terminate their “Zillow Offers” program. They still had a bunch of houses in inventory. 8800 homes as of February 2022. What’s worse is they intend to sell those homes to big Hedge funds and Wall Street types. Likely removing those properties from the market for the long term as corporately held rental properties. To read more on why I think that’s not good for the general public, click here.

You’re telling me the internet can’t solve all my problems?!?

If your telling yourself “I thought Zillow had their poop in a group, how will I ever determine the value of my home now?!?!” don’t you worry. I’ve got a very simple and cost effective solution for you.

Talk to your friendly neighborhood Realtor.

As Realtors we are actively involved in the market on a daily basis. We see all kinds of homes in varying conditions, locations and price points. This gives us a back log of knowledge to fall back on when determining any particular homes value.

Time to unplug and talk to a human

Some of the things we’re looking at are location, condition, amenities, upgrades, bedroom count, bathroom count, square footage and most importantly, comparable sales data. The more recent that sales data the better. We’re currently in an up trending market. Meaning if a home sold a year ago for 200k then it should sell for more today. This is assuming all the other variables are the same. The tricky part is when the variables change, which I will admit is more often than not. That’s why it’s important to work with someone that has experience in this arena.

We can’t speak for all Realtors, but this is a service we provide for free. If you’re simply trying to determine a homes value we’re happy to determine that value for you. We’re just hopeful that when the time comes to sell you remember who helped you out (hint hint, nudge nudge).

I hope that this article has armed you with a little bit of knowledge on why your “Zestimate” might be a bit off or WAY off. I will admit that they do sometimes get it pretty close. More often then not though, they usually need some adjustment.

If you’re curious to know what your homes value is or how far off your “Zestimate” is, feel free to reach out to either of us. We’d love the opportunity to assist you.

-Cody & Jos-

First Time Home Buyers vs Wall Street

What The Heck is a “Hedge Fund” Anyway?

I’ve made an observation over the past couple of years that has peaked my interest. Large Hedge funds and Wall Street types buying up single family homes. Now, I’m by no means a seasoned investor in the stock market but I’d like to think I know a thing or two about the benefits of home ownership along with investing in real estate. So I dug a bit deeper. Why is Wall Street playing around with single family homes?

Home ownership has long been a cornerstone of the American Dream, but recent trends show that hedge funds and institutional investors are buying up a large portion of these homes. If you’re paying attention to the news you’ll hear about company’s like “Blackstone”, “JPMorgan” and even “Zillow” buying up homes in various Metropolitan markets around the country. Places like Atlanta, Phoenix and Los Angeles. To the best of my knowledge they haven’t trickled down to the smaller markets yet, but only time will tell on that one.

I thought this was a fairly recent trend since it was getting all kinds of media attention, but after reading more into it I found out that Institutions have been doing this in some capacity since the 1960s. Usually this was more focused on larger commercial developments like hotels, apartment complexes, shopping malls, you get the picture. Wall Street started investing in single-family rental homes in the mid-2000s, but really picked up steam right at and shortly after the 2008 housing crash. They saw an opportunity to buy an “Asset” that, generally speaking, appreciates in value and throws off cash flow. Much like a bond or dividend paying stock. But, with the benefit of being a tangible asset that’s also a great hedge against inflation.

What does this mean for you as a first time home buyer?

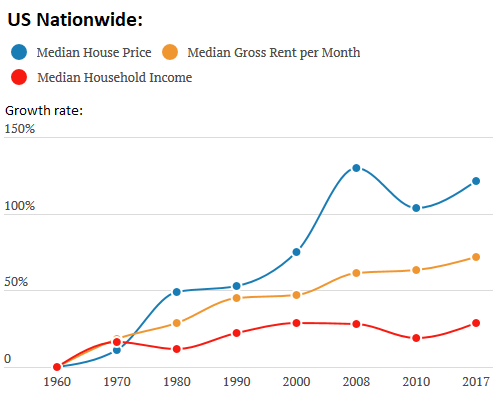

To help unpack what this all means I think it helps to look at some stats on home ownership costs, rental costs and median income rates over the last 70 years. I think this helps to illustrate the motivations of the smart money folks trying to capitalize on home ownership.

Just in case you’re not a graph nerd like I am let me break it down for you. Based on Census data going back to 1960 for median household incomes, median gross rents per month, and median house prices, all adjusted for inflation, it shows that nationally, incomes since 1960 have risen just 29%, while rents have risen 72%, and house prices have soared 121%.

Long story short: your parents and grand parents probably had an easier time affording a home than you probably will. Now that’s not to say they didn’t have their own challenges. Depending on when they bought they may have paid as much as 18% interest rate on their mortgage. All the sudden that high 5% to low 6% rate doesn’t seem that bad.

Now let me just say I don’t have a crystal ball. I can’t predict the future. What I can do is take a look at the data and try to come to some sort of conclusion. If you take a look at the blue line on that graph you can see that it’s had a pretty steady upward pattern. Even if you take out the aggressive rise and fall between 2000 and 2010 (the housing crash of 08) it still shows a a pretty steady increase. That’s home values.

Furthermore, the yellow line that represents the average rental rate also shows a pretty steady increase. The red one which represents wages is relatively flat compared to the other 2…

Based on what I see in this graph coupled with the actions of all these institutional investors, I’d be willing to wager that Wall Street is betting on home affordability being out of reach for a lot of Americans given a long enough time frame and the “Status Quo” not changing. I believe they want you to be a renter for life. A renter nation. As someone that takes great pride in helping people achieve their dreams of home ownership, this is a sobering realization to come to. This isn’t new information though and I’m certainly not the only person to draw a conclusion like this.

Putting the “Wind Back In Your Sails”

If I haven’t dashed your dreams of home ownership yet, stay with me! This is where we stick it to the man!! Just because it’s pricier to buy a home now than in the past doesn’t mean you can’t do it! There are all kinds of creative ways to get you into your first home.

Low down payment options

As a first time home buyer it’s likely that the biggest problem you’ll have owning a home is the down payment. There’s a lot people out there that think you need to have 20% down to buy a home for you to live in. That simply isn’t true. The Federal Housing Administration or FHA will do loans for as little as 3.5% down. Even if you don’t have great credit!

If you’re ok with living a bit out out of town you could also qualify for a 0% down USDA loan. Think small town America where you know everyone. I grew up in a small town and wouldn’t change a thing about my up bringing.

If you served in the Military you qualify for a VA loan which is also a 0% down loan. If that’s you, Thank you for your service!

Even the standard conventional loan you can do as low as 5% down. There are also low income grants available to you depending on your income level. This is by no means a comprehensive list of all the financing options available to you, and frankly, that topic deserves its own blog post (I think I just came up with my next article lol…)

House Hacking

If you’re a reader or listener to “Bigger Pockets”, a real estate investing podcast/website/community, than you’ve heard this word. For the uninitiated, “House Hacking” is a creative way to help offset the cost of your home. This is a method I’ve used in the past and always encourage any of my clients to try that are willing to think outside the box.

Probably the most common way to do this is to buy a live in duplex. A Duplex is a 2 unit housing structure situated on a single parcel of land. They’re very similar to townhomes but differs in that it has multiple attached units on one piece of property. Unlike a townhome which has 1 unit on one parcel of ground. It’s a pretty simple strategy really. Live in one unit and rent out the other unit. Depending on how good of a deal you get you could potentially live in the unit for free. Couple this method with the use of Airbnb and/or roommates and it’s not outside the question to actually get paid to live in your house.

What’s really cool about this strategy is you can use an FHA loan to get into a duplex house. As a matter of fact you can even buy up to a 4 unit apartment building with this 3.5% down financing strategy. The only kicker is you MUST occupy the property for a minimum of 1 year.

Buying a “Fixer Upper” (Definitely not this one though…)

If you’re a bit handy (or don’t mind watching youtube on how to do home remodel projects) than this may be a great way for you to score a good deal. This can potentially get you a house in a neighborhood you might not have been able to afford otherwise. This is a method I’ve personally used to great success. As a matter of fact, I don’t think I’ve ever bought a “nice” house. My wife tells me the next one we buy has to be a nice one though lol… The uglier the better in my opinion.

Now there are limits to this. As a first time home buyer I wouldn’t recommend buying a home with extensive foundation problems. That can get very expensive very quickly. Try to find that ugly duckling with good bones. At the end of the day there is always a price where any home, no matter how bad it is, makes sense. The real question is whether or not you can get it bought at a price that makes sense. As a first time buyer that’s why it’s so important to align yourself with a knowledgeable Realtor. Which segues really nicely into my next point….

Find a Knowledgeable Realtor

Now I might be a bit biased but I firmly believe that working with a knowledgeable Realtor is crucial. ESPECIALLY if this is your first home purchase. All of these strategies I listed above are great. I highly recommend them, but if you end up buying the wrong property or don’t understand the ins and outs of these strategies you could end up getting burned.

The last thing you want is to over pay for a property, over estimate the rents a property can command or under estimate the cost of a remodel. That’s why its critical to work with someone with experience in all these areas. Especially if you need to implement these strategies to make buying a home within your grasp. They will act as your guide to help you along in your adventure of home ownership.

Follow the Smart Money

I can’t say for sure that all the doom and gloom I talked about above will come to pass in our lifetime. I certainly hope that it doesn’t. I firmly believe in the idea of the “American Dream” of home ownership. If you want to own a home, there is a way to make it happen no matter your circumstances. If buying a home is something you’ve always thought is out of reach, I hope this article has armed you with helpful insight and outside the box methods to make that within reach for you. Wall Street seems to think it’s a good idea, why shouldn’t you?

As always, if any of the ideas and strategies in this post have piqued your interest, don’t hesitate to reach out to either of us.

-Cody & Jos-

Buying a Home – 10 “Easy” Steps

Yay!! You’re thinking about buying a home!

Purchasing a home is a huge step in life and a giant financial investment. Often times, it’s the single largest purchase that most of us will make in our lifetime. But, it doesn’t have to be a complicated and stressful process. With the right knowledge and guidance, you can make the process smooth, easy and even fun! Here are the ten steps you need to follow to purchase your dream home:

Get Pre-Approved

- The first step is to get pre-approved for a mortgage. This will give you an idea of how much you can afford and make you a more attractive buyer to sellers. It’s our recommendation you don’t even view a home without having a pre-approval in hand. You can always window shop on websites like Zillow, Realtor or hey, here’s an idea, even our personal website! But until you have a lender letter in hand, please stick to online searches. Besides, getting pre-approved will also give you a reason to brag to your friends about your credit score.

Meet With Your Agent

2. After you have your pre-approval, it’s time to find a real estate agent if you don’t already have one. If you haven’t found one yet, we’re always open to helping new clients! We will help you find homes that fit your budget and preferences and guide you through the buying process, and also serve as your personal tour guide.

Start Looking For Homes

3. This is where the real fun begins! With the help of your agent, (hopefully us) start looking at homes that meet your criteria. Take the time to visit several homes and make sure you find one that you love, and that has the perfect spot for a home theater you’ve always wanted!

Make An Offer

4. Once you’ve found a home, it’s time to make an offer. Your agent will help you determine a fair price and negotiate with the seller on your behalf, and also help you to haggle like a pro. They will also walk you through all the paperwork so you understand everything you’re signing.

Offer Accepted

5. After the offer is accepted, you and the seller will sign a purchase agreement. At this point you’ll be what’s called “under contract” to purchase. This means you intend to purchase the property on a pre-determined date you and the seller mutually agree on for a price and terms agreed upon by both parties.

Inspections

6. Before you close on the home, it’s crucial to have it inspected by a professional inspector. We generally have this done within 14 calendars days in our market. This will ensure there are no hidden issues with the home, or any haunted rooms. Just in case there are issues, this is where we get to negotiate the repairs of the home. In some cases when the repairs are too extensive, you can always walk away from the transaction as well. This is where having a great real estate agent that puts your needs first is critical.

Appraisal

7. The lender will also require an appraisal of the home to ensure the purchase price is fair market value. This is also the time to make sure your house doesn’t have a value lower than your car.

Title Search

8. The title company will perform a title search to ensure there are no liens or other issues with the property’s title. This is also the time to make sure your house is not haunted by a previous owner’s ghost.

Documents To Lender

9. The lender will require various documents, such as proof of income and employment, before they approve the loan. This is also the time to make sure you didn’t forget to change your name to “Duke of Bucks”

Closing Day

10. Once all the steps are complete, you will close on the home. This typically involves signing ALOT paperwork and paying closing costs. Make sure you’ve got your signing hand good and ready! It might be sore by the end of it! This is also the time to finally put that “Home Sweet Home” sign on the front lawn.

By following these ten steps, you can purchase your dream home with little to no stress. Don’t get us wrong, buying a home can be an emotional process with peaks and valleys throughout. But if you’re working with an experienced real estate agent they will have your back through thick and thin, and even have someone to laugh with when things get overwhelming. If you’ve been kicking around the idea of buying your first home or you 20th, give us a call and we’d love to get you on the right track!

-Cody & Jos-

Own vs. Rent – 7 Benefits of Home Ownership

So you’re thinking about buying a home?

Homeownership has long been considered a rite of passage and a symbol of financial stability. The “American Dream” if you will. There are many benefits to owning a home, as opposed to renting one. In this blog post, we will discuss seven of the most significant benefits of home ownership.

EQUITY

- One of the biggest benefits of home ownership is the ability to build equity in the property. As you make mortgage payments, you are paying down the principal of the loan and building equity in the property. This equity can be used as collateral for future loans, or it can be accessed through a home equity loan or line of credit. This is a great strategy if you plan to accumulate rental properties and a strategy Cody and I use to snowball our portfolio (more on that in a different article).

TAX BENEFITS

2. Owning a home also comes with certain tax benefits. The interest paid on a mortgage is a tax write off, which can result in significant savings on your annual tax bill. Additionally, property taxes are also tax-deductible.

FORCED SAVINGS

3. Another benefit of home ownership is that it can act as a forced savings plan. Each month, some of your mortgage payment goes towards paying down the principal of the loan, which is like money being saved in the form of equity.

STABILITY

4. Homeownership provides a sense of stability and security. Renters are at the mercy of landlords and can be forced to move at the end of a lease. They’re also subject to rent increases, which we have been seeing a lot of lately. Homeowners have the security of knowing that they will have a place to live for as long as they wish, as long as they can make their mortgage payments.

PRIDE OF OWNERSHIP

5. Homeownership also provides a sense of pride and accomplishment. When you own your home, you can decorate and make changes as you see fit. You can take pride in the fact that you have a place of your own.

APPRECIATION

6. Another benefit of homeownership is the potential for appreciation of the property. Real estate values typically increase over time, which can result in significant financial gain for the homeowner. Particularly if you plan to stick around for a while!

COMMUNITY

7. Homeownership can also provide a sense of community. When you own a home, you are more likely to be invested in your community and to get involved in local activities and events. Some of our best friends are the neighbors we live next to.

In summary, homeownership has many benefits over renting. Now I know we may be a bit biased since we eat and sleep real estate, but home ownership isn’t for everyone… If you have to move around frequently and don’t want to keep every house you buy for longer than 5 years, we wouldn’t recommend buying under those circumstances. Additionally, if you like having the comfort of knowing you’ll never be in charge of fixing anything, Home ownership might not be for you.

If you’ve been kicking around the idea of buying yourself a home, please feel free to reach out to either of us. We can discuss the pros and cons and find out whether home ownership is a good idea for you!

-Cody & Jos-